Goldman Sachs slashed its year-end gold price target by $500 to $4,900 per ounce on June 19, 2026, walking back its earlier $5,400 conviction call. The bank also abandoned the Federal Reserve rate-cut thesis that had underpinned the bank’s entire commodity bull case, a revision that arrives with gold spot trading in the low $4,300s. Bitcoin itself is navigating one of the most consequential macro inflection points of the current cycle.

The downgrade is not a routine target trim. Goldman’s commodity team had progressively raised its gold forecast through late 2025 and into January 2026, citing structural central bank buying and an expected 100 basis points of Federal Reserve easing by mid-2026.

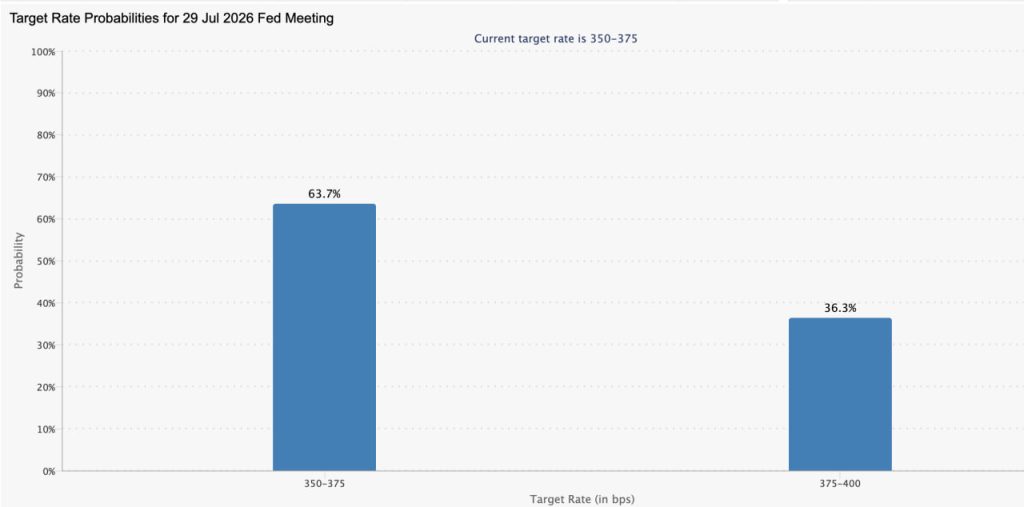

With the Fed now expected to hold rates steady through the end of 2026, the rate-cut pillar of that thesis has collapsed entirely, and the market implications extend well beyond the gold desk.

The Fed’s new hawkish reality just forced Goldman Sachs to slash its gold forecast by $500 https://t.co/DQwpfYmBlN

— MarketWatch (@MarketWatch) June 19, 2026

Goldman Sachs Revised Call: What the $500 Target Cut Actually Reveals About the Fed Hold Thesis

Goldman’s original bullish framework rested on three structural pillars: Federal Reserve rate cuts totaling roughly 100 basis points by mid-2026, which would compress real yields and drive Western ETF inflows into gold; structural central bank buying running at approximately 760 tonnes per year, nearly double the pre-2022 norm of 400–500 tonnes annually; and private-sector portfolio diversification into gold as institutional allocators sought a macro hedge against dollar debasement. All three were supposed to compound simultaneously.

The rate-cut pillar contributed the most directly to Goldman’s ETF inflow projections, which the bank estimated at roughly 360 tonnes for 2026. When the Federal Reserve signaled a higher-for-longer posture, Goldman Sachs commodity team, led by Daan Struyven, recalibrated the inflow assumption downward, producing the $500 target reduction.

Goldman cuts gold target by $500 → $4,900 (from $5,400)

Reason: Fed no longer seen cutting rates in 2026 — Warsh's hawkish debut this week

Goldman: every 50bps of cuts = ~$120/oz support | removed half-point of easing from model

Still implies gains in H2 2026 — just smaller |… pic.twitter.com/v2v32Y7mmc— Line Avenue (@xipixamamy) June 19, 2026

The bank had described the rally as driven by “sticky and structural buying” and said upside risks to $4,900 were rising, language that has now been reversed.

The central bank buying pillar remains intact but insufficient on its own. Goldman’s updated 2026 estimate puts central bank purchases at approximately 60 tonnes per month, down from 80 tonnes in 2025, as emerging-market reserve managers continue to diversify away from dollar-denominated assets.

That structural demand provides a floor, Goldman’s bear case sets gold at $4,400 if the Fed unexpectedly resumes hiking, but it cannot single-handedly offset the loss of rate-sensitive Western ETF inflow momentum.

What ‘No Fed Cuts’ Actually Means for Bitcoin: The Transmission Path

The transmission mechanism from a Federal Reserve hold to Bitcoin runs through three sequential channels. First, elevated real yields make dollar-denominated cash instruments more competitive against non-yielding assets, a dynamic that structurally pressures both gold and Bitcoin simultaneously. Second, a stronger dollar environment, which a higher-for-longer Fed typically sustains, historically correlates with compressed risk appetite across speculative assets.

Third, and most directly, Bitcoin ETF inflows have been partly driven by the same macro narrative Goldman’s gold thesis relied on: falling real yields and dollar softening as catalysts for institutional reallocation into alternative stores of value.

Bitcoin ETF flows are already sensitive to this rate calculus. Previous analysis has documented how the ETF outflow dynamics and liquidity challenges tied directly to the higher-for-longer rate environment created sustained redemption pressure during prior Fed hold periods, with institutional allocators rotating back toward yield-bearing instruments. A Fed that stays on hold through December 2026 extends that headwind by at least two more FOMC cycles.

Goldman’s bear case for gold, the $4,400 scenario triggered by a Fed rate hike, carries the most severe read-through for crypto. A resumption of Fed tightening would signal a liquidity contraction that historically drains speculative capital from digital assets ahead of traditional safe havens, as margin calls and risk-off positioning hit higher-beta assets first. That scenario is not Goldman’s base case, but the bank explicitly flags it as a tail risk in the same note that produced the target downgrade.