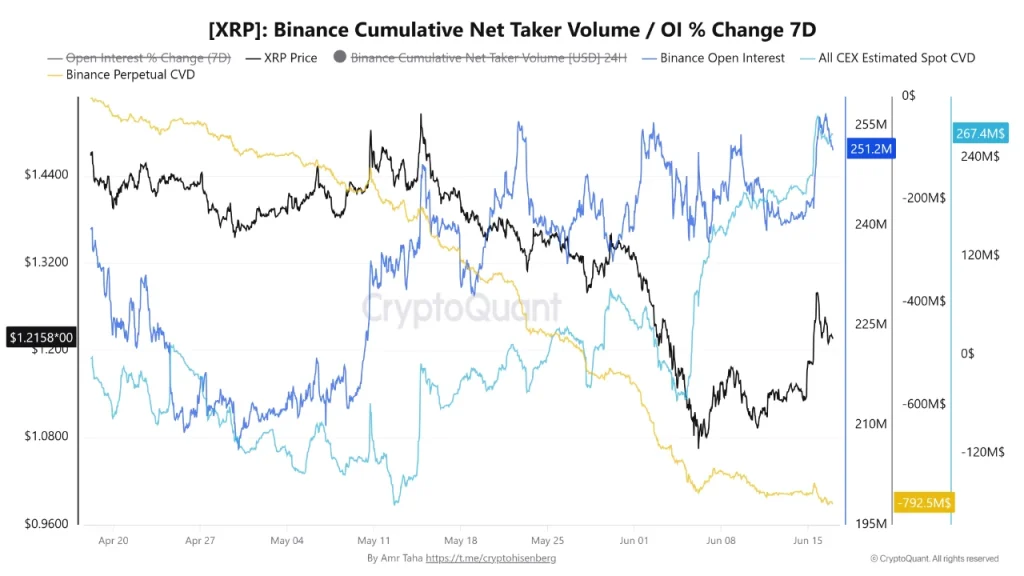

XRP News: XRP price has reclaimed the $1.17 price level with All CEX Estimated Spot CVD climbing to $267.4 million, its highest reading since mid-May, while Binance Perpetual CVD simultaneously crashed to a record low of -$792.5 million.

That combination of figures, drawn from on-chain analysis tracked by CryptoQuant analyst Amr Taha, marks one of the sharpest divergences between spot and derivatives positioning in XRP’s recent history.

The signal is analytically significant not because either metric in isolation tells a complete story, but because their simultaneous extreme readings create a structural tension the market cannot sustain indefinitely.

According to Taha, the current setup echoes configurations observed near two prior local lows, where the same tug-of-war between accumulating spot buyers and entrenched derivatives sellers preceded a sharp directional resolution.

The open question the market must now resolve is whether the weight of record short positioning in perpetual futures triggers a short squeeze that drives XRP toward $1.28–$1.51, or whether spot demand exhausts itself and price revisits the $1.14–$1.11 support band.

XRP News: What the Spot CVD and Perpetual CVD Actually Reveal About Structural Market Tension

Digging deeper into the XRP news, context significantly enhances the raw figures. All CEX Estimated Spot CVD is a cumulative measure of net buyer-initiated volume across centralized exchange spot markets. When it rises, genuine market participants are paying the ask, absorbing available sell-side liquidity with real capital.

The figure reaching $267.4 million is not a projection; it represents a measurable accumulation of spot demand across CEXs, reversing sharply from the -$177 million reading recorded on April 12, a swing of more than $444 million in net spot flow direction over roughly two months.

Binance Perpetual CVD measures something categorically different: the net directional bias of derivatives traders using perpetual futures contracts on Binance, where no underlying asset changes hands.

A reading of -$792.5 million means that, cumulatively, sell-initiated volume in Binance perpetual futures has overwhelmed buy-initiated volume by that margin; derivatives traders are net short at a record scale. This is the distinction that matters: spot CVD reflects genuine ownership demand, while perp CVD reflects leveraged directional bets that can be unwound instantly without moving underlying supply.

The causal chain that creates squeeze risk runs as follows. Spot buyers accumulate XRP across CEXs, gradually tightening available float. Simultaneously, derivatives traders on Binance build record short exposure through perpetual futures.

As spot demand firms the price, short positions move into a loss. Forced liquidations or voluntary short covering then require those traders to buy back their positions, adding upward price pressure on top of existing spot demand and creating the feedback loop that defines a short squeeze.

The cumulative short liquidation leverage stacked on Binance USDT perpetuals has been estimated at approximately $227.1 million versus only $24.0 million in long liquidation leverage, a roughly 90% short-skew that quantifies exactly how asymmetric the squeeze risk is.

The two prior analog setups Taha references are important for calibrating expectations. In the April episode, All CEX Estimated Spot CVD climbed from roughly $1.08 billion to $1.39 billion between April 2 and April 24, while Binance Perpetual CVD deepened from approximately -$65 million to -$392 million – a divergence that resolved with price finding a local low and staging a recovery.

An earlier setup showed Binance Spot CVD near $520.2 million against a perpetual CVD near -$261 million as XRP consolidated around $1.32, before a directional break occurred. What those analogs confirm is that this divergence pattern is structural and repeating, not a one-off anomaly.

What they cannot confirm is which direction the current iteration resolves, both prior cases involved eventual price recovery, but the timeframes and triggers differed, and the current perp CVD reading is materially more extreme than either precedent.

Exchange withdrawals rising to 53.1% on Binance adds a layer of nuance. When tokens leave exchanges, they reduce immediately available sell-side liquidity – a dynamic that, combined with spot accumulation, compresses the float that short sellers could borrow against or that spot sellers could dump into.

The enterprise adoption momentum building through RippleNet provides a fundamental backdrop that may be encouraging longer-term holders to withdraw and hold rather than trade, but that interpretation remains speculative without deeper wallet-level data.