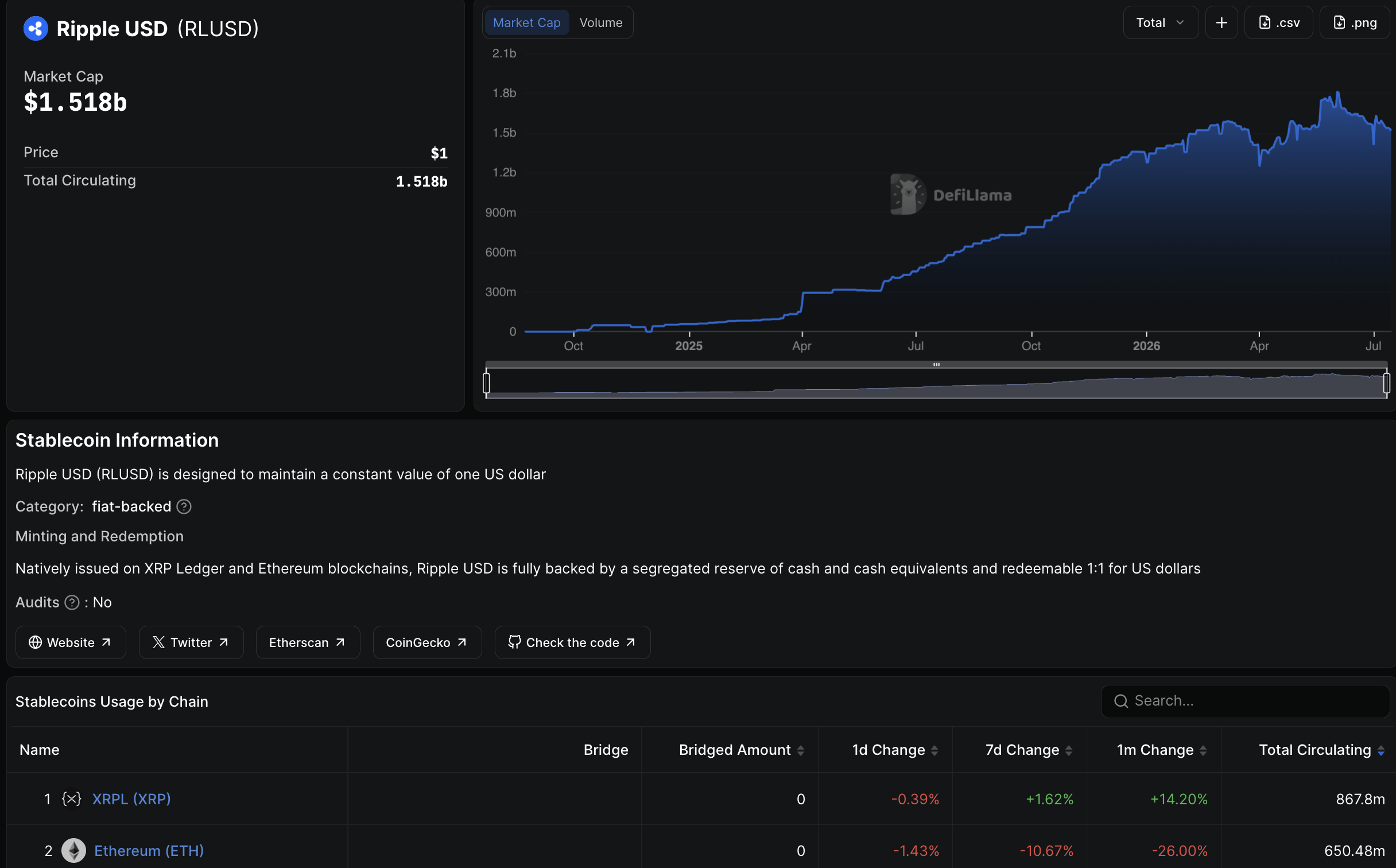

In XRP news today, Ripple’s RLUSD stablecoin has shifted $871M, 57% of all RLUSD, per XRPScan, onto the XRP Ledger, which overtook Ethereum as RLUSD’s main network in late June 2026. The shift matters because it puts real institutional money back on the chain XRP secures.

Nearly $900M now generates fees, liquidity, and settlement activity. That deployment follows Ripple’s MiCA approval in July 2026 and the launch of a JFSA-regulated RLUSD in Japan with SBI Group.

There is also the August 7, 2025 closure of the SEC lawsuit, the legal clearance that made licensed institutional deployment on XRPL viable for the first time in five years.

The open question the market must now resolve is whether the RLUSD migration’s fee-burn and DEX-routing mechanics represent the structural demand catalyst XRP has needed, or whether the substitution effect, routing institutional capital into the dollar-pegged stablecoin rather than through XRP itself, continues to cap the token’s price recovery despite the on-chain signal.

XRP News and On-Chain Mechanics: What the $871M Migration Actually Reveals About XRP Structural Demand

Ethereum’s RLUSD balance peaked at $1.25Bn on March 12, 2026, but has since declined 47% to $660M. This drop isn’t due to mass redemptions; total supply data shows aggregate supply remained near $1.53Bn. The difference has migrated to XRPL, which now leads after a crossover in late June.

Three on-chain mechanics enhance XRP utility from this migration. First, every RLUSD transaction on XRPL incurs a small XRP fee, which is burned with each transfer.

Second, holding RLUSD on XRPL requires accounts and trustlines that lock XRP in reserves, increasing institutional XRP holdings.

Third, RLUSD trades against XRP on the ledger’s exchange, creating a significant native dollar pair. If RLUSD supply continues to shift and transaction volume scales proportionally, there will be measurable on-chain demand for XRP.

Regulatory Rails: What the MiCA Approval and SBI Launch Actually Reveal About Licensed Institutional Scale

The RLUSD migration is closely tied to Ripple’s regulatory framework, with MiCA approval secured in July 2026 and the launch in Japan alongside SBI Group. This collaboration benefits from SBI’s established infrastructure, which many stablecoin issuers lack.

The regulatory context favors control over licensed payment flows, and Ripple has integrated both XRP and RLUSD into corporate treasuries, creating ongoing demand for XRP.

The launch of JFSA-regulated RLUSD follows the SEC case’s settlement on August 7, 2025, enabling greater institutional deployment on XRPL. This resolution provided the necessary clarity on compliance for routing licensed payments through XRP.

The RLUSD migration marks the first significant capital deployment since the SEC lawsuit’s resolution, using verifiable on-chain transactions rather than relying solely on partnerships.

Ripple Receives Full MiCA CASP License, Gains EEA-Wide Crypto Services Approval

Ripple announced it has received full Crypto Asset Service Provider (CASP) authorization under the EU’s MiCA framework from Luxembourg’s CSSF. The approval follows its preliminary authorization in… pic.twitter.com/JGokDaFQzU

— Wu Blockchain (@WuBlockchain) July 6, 2026

The Substitution Tension: What RLUSD’s Settlement Role Actually Reveals About XRP’s Bridge Asset Problem

In other XRP news today, the utility of XRP as a cross-border bridge currency for MoneyGram, banks, and remittance firms created direct demand for it.

However, RLUSD, a dollar-pegged stablecoin that settles institutional payments on XRPL, may fulfill that same role, allowing institutions to use the XRP Ledger without holding much XRP.

By 2026, the stablecoin market dynamics highlight that every RLUSD transaction that consumes XRP for fees and reserves does not displace XRP demand but can generate it, albeit in small amounts with current volumes.

The key issue lies in transaction volume data rather than supply. For RLUSD to enhance XRP demand significantly, high-frequency institutional transactions must lead to meaningful XRP consumption through fees and reserves.

Until then, the risk of substitution remains unless on-chain data shows RLUSD’s impact on XRP demand is substantial.