The stablecoin market cap shed $7.7Bn in June 2026 alone, the largest single-month dollar decline since May 2022’s Terra-Luna collapse triggered crypto winter, bringing the total drawdown to roughly $10Bn since the May peak, according to RWA.xyz data.

On a percentage basis, the contraction amounts to approximately -3%, a figure that bears no structural resemblance to the -26% wipeout recorded across the 2022 bear market.

Paul Howard, senior director at trading firm Wincent, framed the pullback directly: “The recent decline in stablecoin market cap represents a relatively small pullback in what we believe is a long-term growth market.”

The open question the market must now resolve is whether this contraction marks a temporary liquidity withdrawal in a long-term growth market, or an early signal that stablecoin dominance is shifting toward regulated newcomers at the expense of incumbent giants USDT and USDC.

Supply Data: What the $10B Drawdown Actually Reveals About Crypto Liquidity in 2026

Context significantly enhances the raw figure. The stablecoin market cap has largely stalled near the $300Bn level since October 2025, the same month Bitcoin hit its $126,000 all-time high, and the June contraction accelerated what had already been a months-long consolidation rather than initiating a new downtrend from a peak.

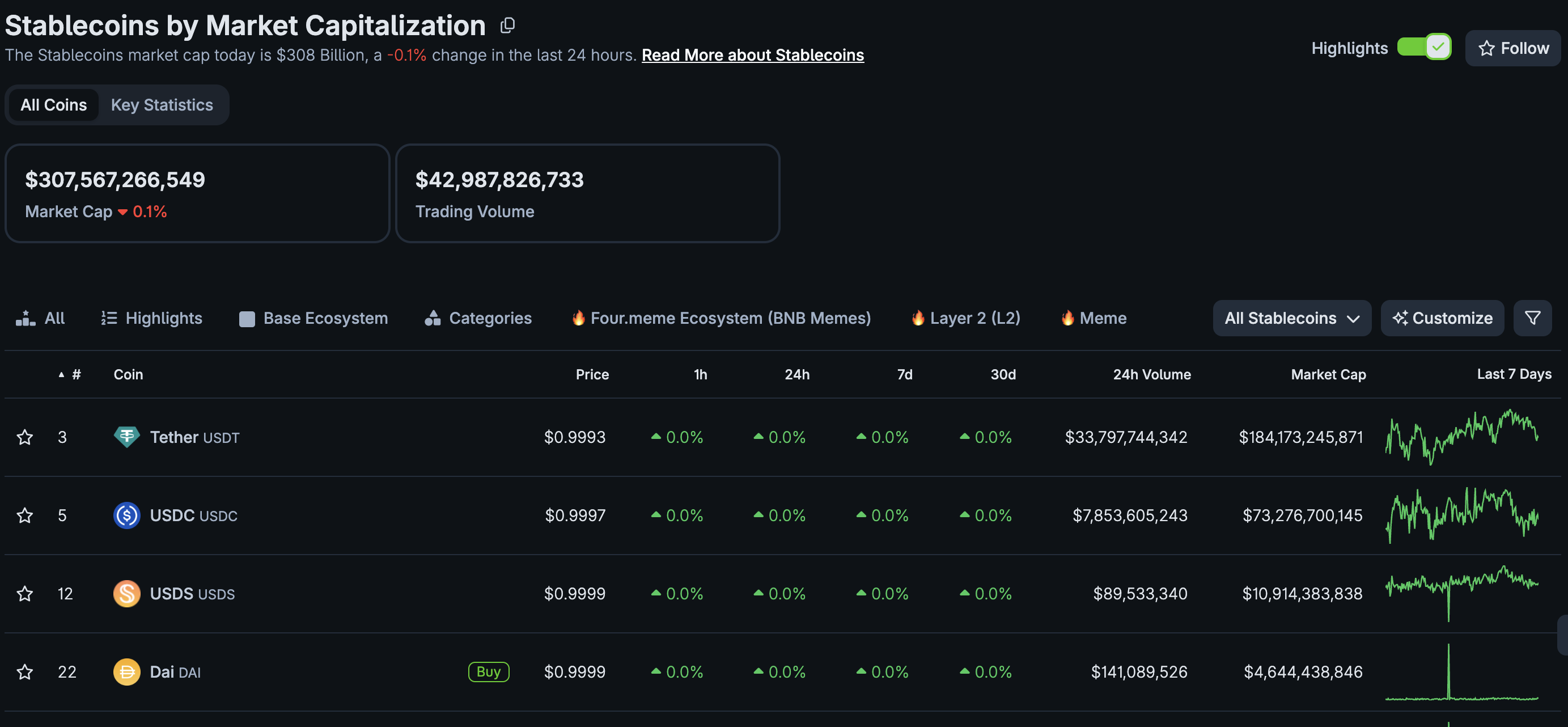

The two dominant issuers absorbed the bulk of the losses. Tether’s USDT, the largest stablecoin by circulation, fell from approximately $190Bn in May to roughly $184Bn by early July, a -$6Bn decline, per CoinDesk Data.

Circle’s USDC dropped from its March 2026 peak of just under $80Bn to approximately $73Bn, shedding roughly $7Bn over a prolonged drawdown.

The percentage comparison to 2022 is the critical frame. During the Terra-Luna collapse and subsequent crypto winter, the combined stablecoin market cap fell from approximately $166Bn in March 2022 to $122Bn by September 2023, a decline of more than 26% over 18 months.

USDC’s descent was particularly severe, falling from $55 billion in July 2022 to below $24Bn by November 2023, compounded by its banking partner Silicon Valley Bank’s collapse in March 2023.

Beneath the headline decline, a competitive rotation is underway. USDG, issued by Paxos and backed by a consortium including Robinhood, surpassed $3.2Bn in circulation. USDGO, issued by Anchorage Digital in partnership with Hong Kong’s OSL Group, nearly doubled to $900M, per CoinGecko data.

The GENIUS Act’s passage created the federal regulatory framework that made these regulated entrants viable, and their early traction suggests the market-share math within the $300Bn total is shifting even as the aggregate figure contracts.

DISCOVER: Best Crypto Presales to Watch Right Now

Why Wincent’s Paul Howard Changes the Risk Reading for Stablecoin Markets Heading Into Q3

Out of 200+ dollar-pegged stablecoins, only a handful will survive the cut.

Paul Howard from @Wincent_co breaks down the upcoming stablecoin consolidation and how the US Clarity Act could be the ultimate catalyst for DeFi.

Full BeInCrypto Podcast drops tomorrow. STAY TUNED! pic.twitter.com/jDlxp1GXCR

— BeInCrypto (@beincrypto) July 1, 2026

Howard added: “Short-term fluctuations in liquidity are normal, but they don’t change our view that stablecoins will continue to play an increasingly important role in the digital asset ecosystem.”

That framing carries weight precisely because it situates the June decline within a cyclical context rather than treating it as structurally significant.

Between December 2025 and February 2026, stablecoin supply fell by roughly $9Bn before bouncing to a new record, a near-identical drawdown magnitude that resolved bullishly within two months.

The broader institutional backdrop reinforces that reading. Citi revised its 2030 stablecoin market cap forecast upward to $1.9 trillion in its base case and $4 trillion in a bull case.

Standard Chartered separately projected a $2 trillion market by 2028. The June contraction runs counter to both projections on a short-term basis but does not challenge the structural thesis behind them.

A more cautious interpretation holds that shrinking aggregate stablecoin supply removes a meaningful tailwind for crypto markets in 2026.

Major stablecoins serve as the primary quote currency for on-chain trading, so a reduction in their circulating supply directly reduces the available dry powder for asset purchases.

A risk-off environment drove redemptions, and if stablecoin supply does not recover ahead of any BTC price rebound, sustaining that rally becomes structurally harder.